Artificial Intelligence

Lending

Trends That Will Shape Lending in 2026

February 23, 2026

Article

CK Editorial Team

4

min read

Lending is entering a moment where speed and compliance have stopped being advantages and started becoming expectations. Lenders no longer are compared only on the basis of products but on experiences. They demand rapid decision fuelled by deep risk intelligence and credit that fits into their business as seamless as a utility.

So What Will Really Shape Lending in 2026?

The defining shift will be whether lenders can operate in real time. The trends shaping lending this year point to one clear reality. Strategy is no longer about choosing which innovations to adopt. It is about building the capability to respond continuously at scale.

The competitive gap continues to widen between institutions that move quickly and those held back by slow change cycles. Let us pinpoint the forces driving this change:

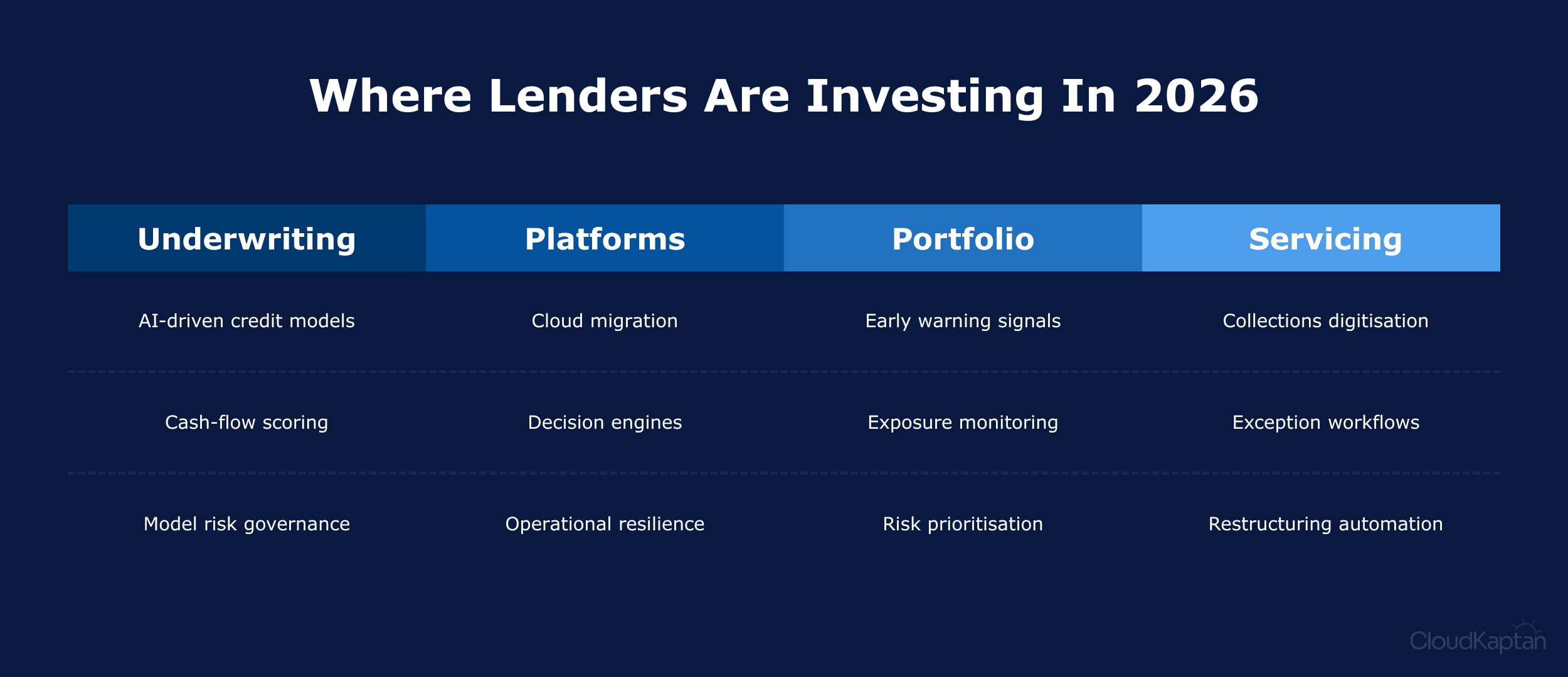

Build AI decisioning for model risk and audit

AI-driven credit decisions are now required to satisfy formal model risk management and supervisory expectations. Lenders are redesigning underwriting architectures to make decisions traceable by default through model lineage, version control, explainability artifacts, and governed GenAI usage. Independent model validation and regulatory review are shaping how AI is deployed, forcing governance, accountability, and human override to be engineered directly into credit decisioning platforms. Lenders must embed governance mechanisms into core processes, not add them later.

Redesign embedded lending for profitability

Credit decisioning will be rebuilt around transaction-level cash-flow data enabled by open banking. Empirical studies and industry implementations show that incorporating income volatility, spending behavior, and liquidity signals materially improves default prediction and risk discrimination compared to bureau-only models, accelerating the shift toward cash-flow-driven underwriting.

Digitise credit exceptions and loan servicing

Digital servicing and exception handling help preserve affordability and borrower resilience after origination. Manual restructures, collections, and policy overrides weaken visibility into repayment capacity and consistent customer treatment. Lenders are embedding rule-based servicing workflows, event triggers, and decision logs to manage stress actions systematically, maintain control over outcomes, and evidence fair, repeatable decisions across the post-disbursal lifecycle.

Shift credit decisioning to cash flow based assessment

Open banking data is now used to understand income stability, spending rigidity, and remaining repayment capacity in near real time. Transaction-level cash flows allow affordability to be monitored beyond origination, revealing volatility and early stress that bureau data misses. This enables credit limits, pricing, and interventions to be adjusted as borrower capacity changes, rather than relying on static, backward-looking credit snapshots.

Use real-time data to detect portfolio risk

Portfolio monitoring can no longer rely solely on bureau-based reviews. Income volatility, spending shifts, and loan stacking appear weeks or months before delinquency is visible. By integrating transaction data across products, lenders can trigger proactive interventions and prioritise risk actions earlier in the cycle, shifting portfolio management from reactive loss response to forward-looking risk control.

Shift toward quality and secured lending in risk-sensitive environments

Growth strategies are prioritizing asset quality by shifting toward secured lending and selective credit. Recent data shows banks and NBFCs increasing exposure to secured products like gold and business loans while pulling back on unsecured credit and new-to-credit borrowers. Gold loans recorded the fastest growth among retail segments, rising sharply and improving portfolio risk profiles as institutions balance growth with risk discipline.

Adopt multi-cloud architectures to manage concentration risk

Multi-cloud strategies is increasingly used avoid concentrating critical credit decisioning, data, and AI workloads on a single provider, reducing operational and regulatory exposure. Decision engines and data layers are increasingly distributed to preserve continuity under outages or third-party disruption. As a result, over 80% of financial services firms now operate with hybrid or multi-cloud environments. Cloud architecture is now designed to protect credit decision resilience, not just efficiency.

Lead the Curve

The trends shaping lending point to a clear inflection point. Future readiness is no longer defined by isolated technology upgrades, but by the ability to execute consistently as markets and customer expectations evolve. Lenders that succeed will be those that design accountable decisioning, gain early borrower visibility, control origination & disbursal actions, and sustain credit decisions reliably.

The next era of technology transformation will be defined by execution. Turning insight into scalable lending capability is where advantage will be created. If you’re assessing how these shifts translate into action for your lending strategy, reach out to us .